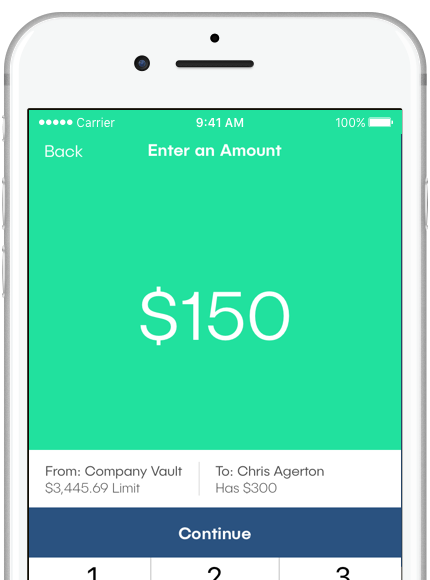

Send

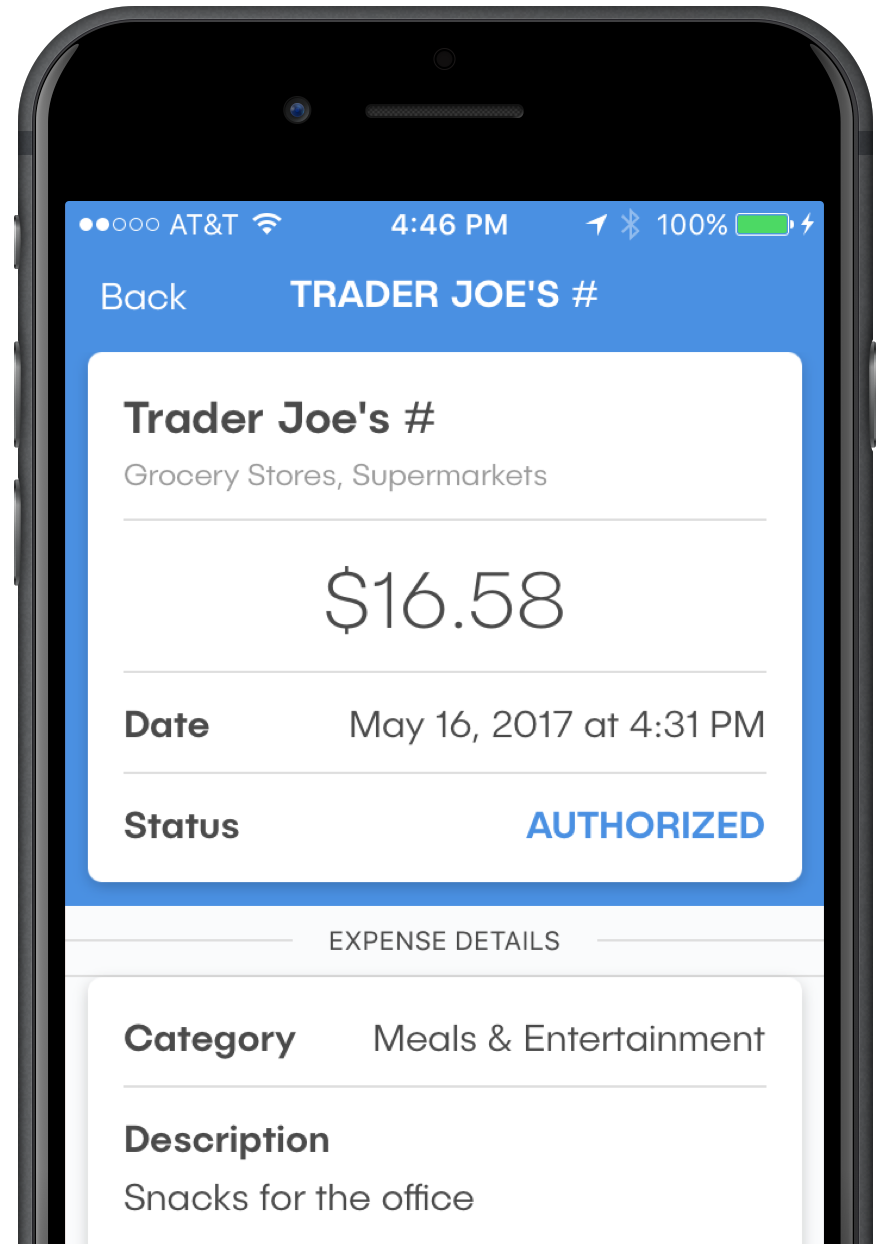

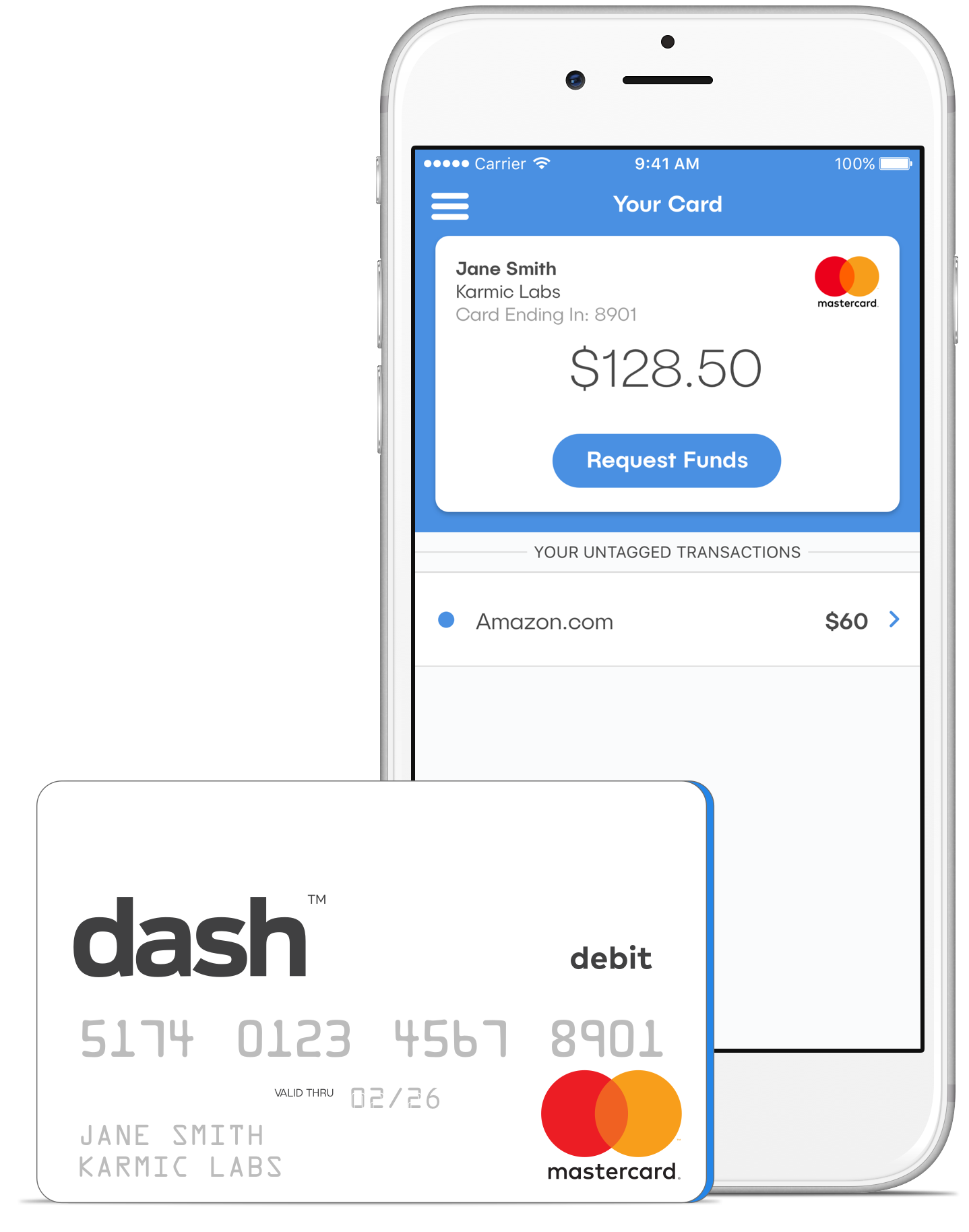

Your business is growing, and your teams need funds to keep it that way. From construction equipment to office supplies, gas to business meals, each team has different needs. Tracking those requests, collecting receipts, and reconciling business expenses can be time-consuming and costly.

With dash, each team member can have access to funds wherever they need them, and business owners and accountants have insight into where those funds are being spent in real time.

Learn more about sending money with dash